Trading

Wednesday, June 17th 2026

Gold: The Safe Haven Whose Options Turned Defensive

GLD options have shifted from steady call skew to put skew after the Warsh nomination, showing a market now paying more for downside protection than upside exposure.

Summary

Gold’s options have shifted from a strong call skew—betting on upside price spikes—to a put skew, reflecting market expectations of downside risk after the nomination of Fed chair Kevin Warsh, which caused a sharp 10% drop in gold. Since early 2024, the 30‑day GLD skew moved from predominantly call‑skewed to put‑skewed on most days, now sitting at +1.15. Implied volatility remains mid‑range, and the put skew is modest compared with equities, indicating a reduced upside bet rather than a crash expectation.

Gold: The Safe Haven Whose Options Turned Defensive

By Tyler Cheves

June 17, 2025

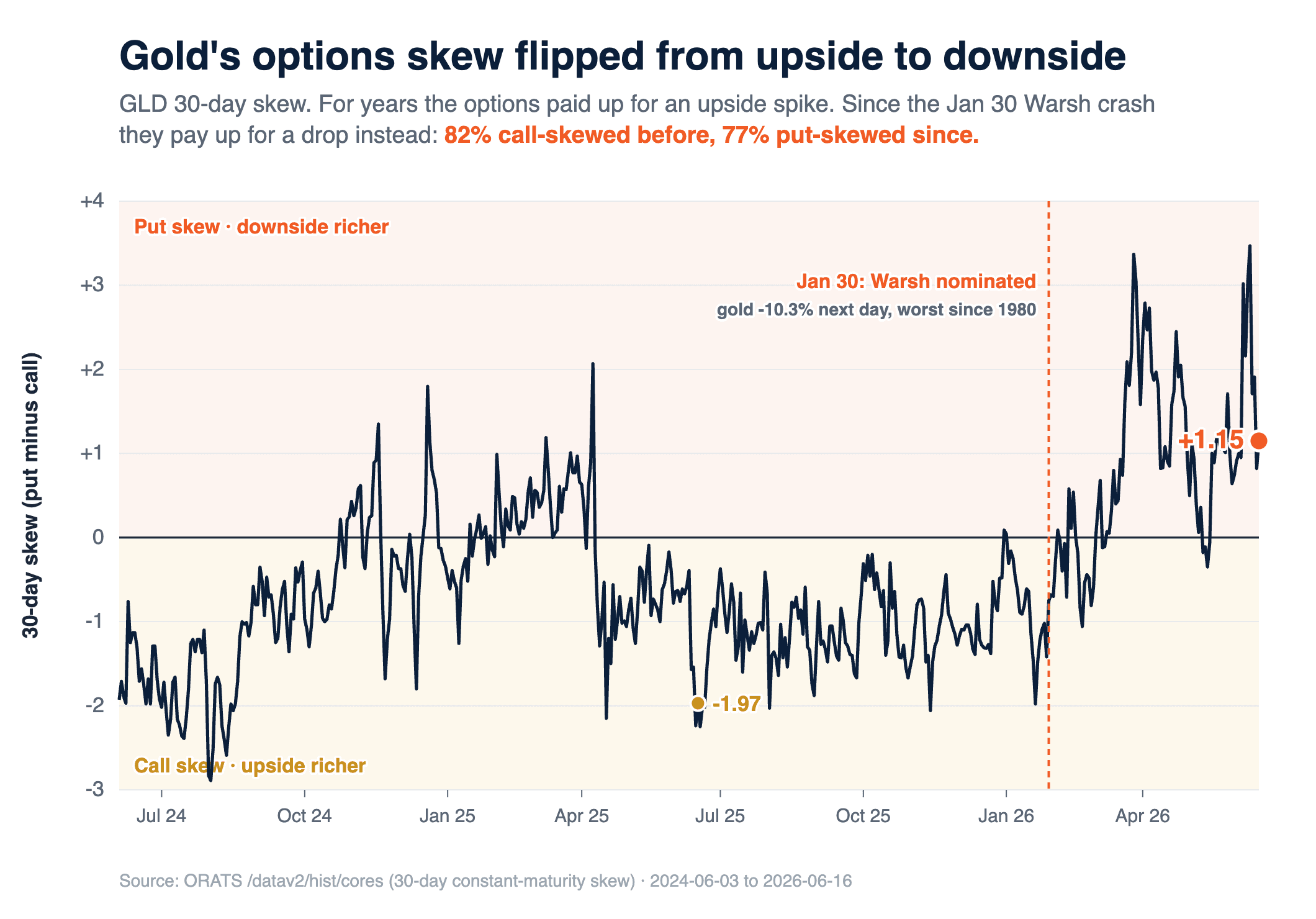

Gold's options have quietly reversed their bet. Across 2024 and 2025 they paid up for gold to spike, the classic call skew of a crisis hedge. Since the January 30 nomination of Kevin Warsh as Fed chair crashed gold roughly 10% in a day, they pay up for gold to fall instead. GLD's 30-day skew was call-skewed (upside richer) on 82% of days before the nomination and has been put-skewed (downside richer) on 77% of days since, and into the June 17 FOMC, Warsh's first meeting, it sits firmly in put-skew territory at +1.15, off the early-June spikes but well above its long-run call skew.

Why gold normally pays for the upside

Stocks almost always put-skew, because the crash is the fear. Gold and most commodities do the opposite and call-skew, because their shocks run upward: a supply scare, a war, a flight to safety. Gold no longer follows that rule.

What flipped gold's skew

Through 2024 and 2025 GLD's 30-day skew sat firmly negative, a steady call skew at -1.97 a year ago. It oscillated for about six weeks after the nomination, then settled into a durable put skew from mid-March on, put-skewed on nearly every day since, +1.15 now.

GLD 30-day skew flipped from call to put after the Warsh nomination

The trigger was violent: gold ran to a record near $495 on GLD on January 29, Warsh was named the next morning, and the metal fell about 10% that session, the worst single day for precious metals since 1980. A hawkish, independent Fed chair is gold's nightmare: higher real yields and less debasement, the opposite of what drove the rally. The options have priced that downside ever since.

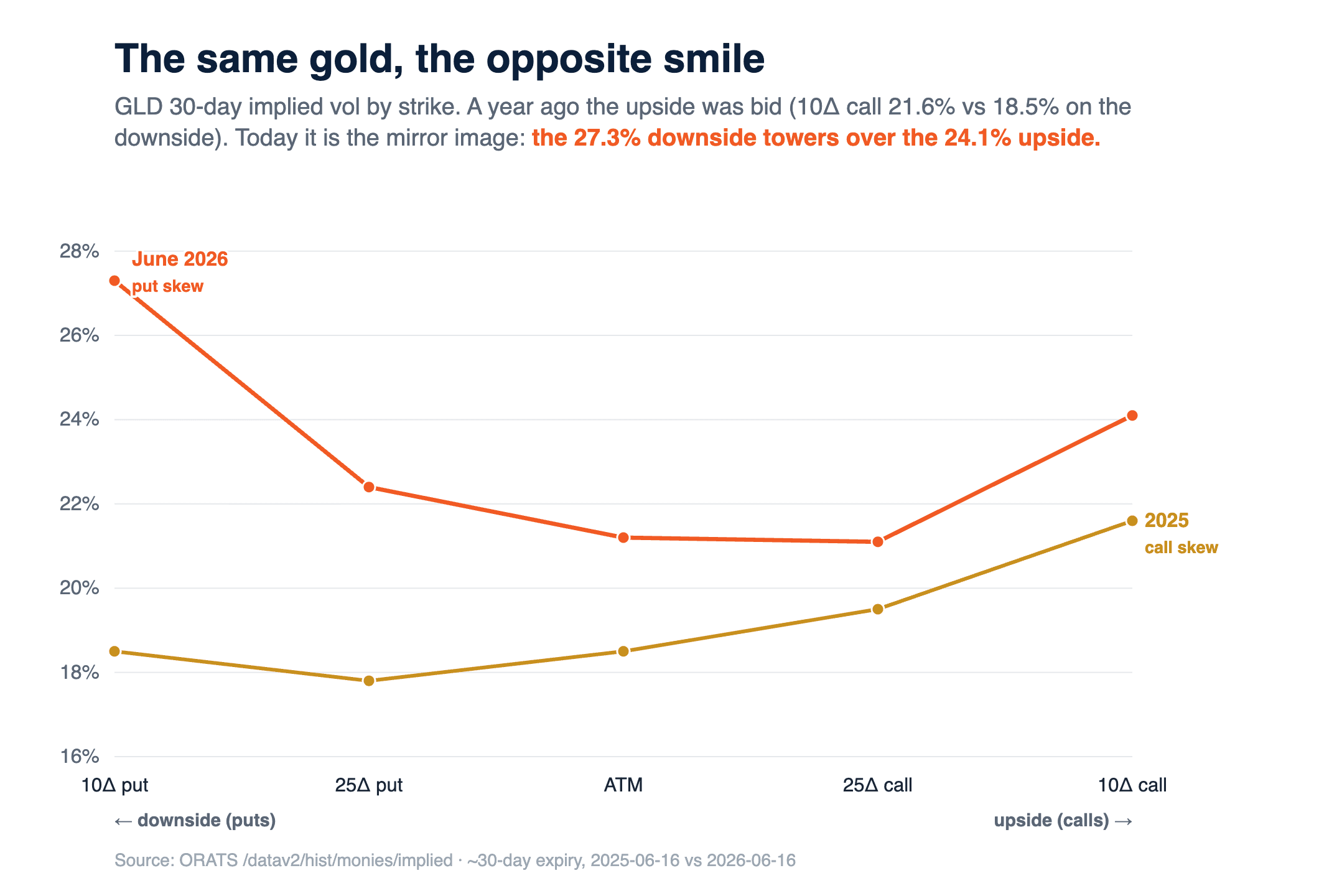

The same gold, the opposite smile

GLD implied vol by strike, a year ago versus now

A year ago gold's 10-delta call implied 21.6% against 18.5% on the downside, so the upside was the bid. Today it is the mirror image: the 10-delta put implies 27.3% against 24.1% on the calls.

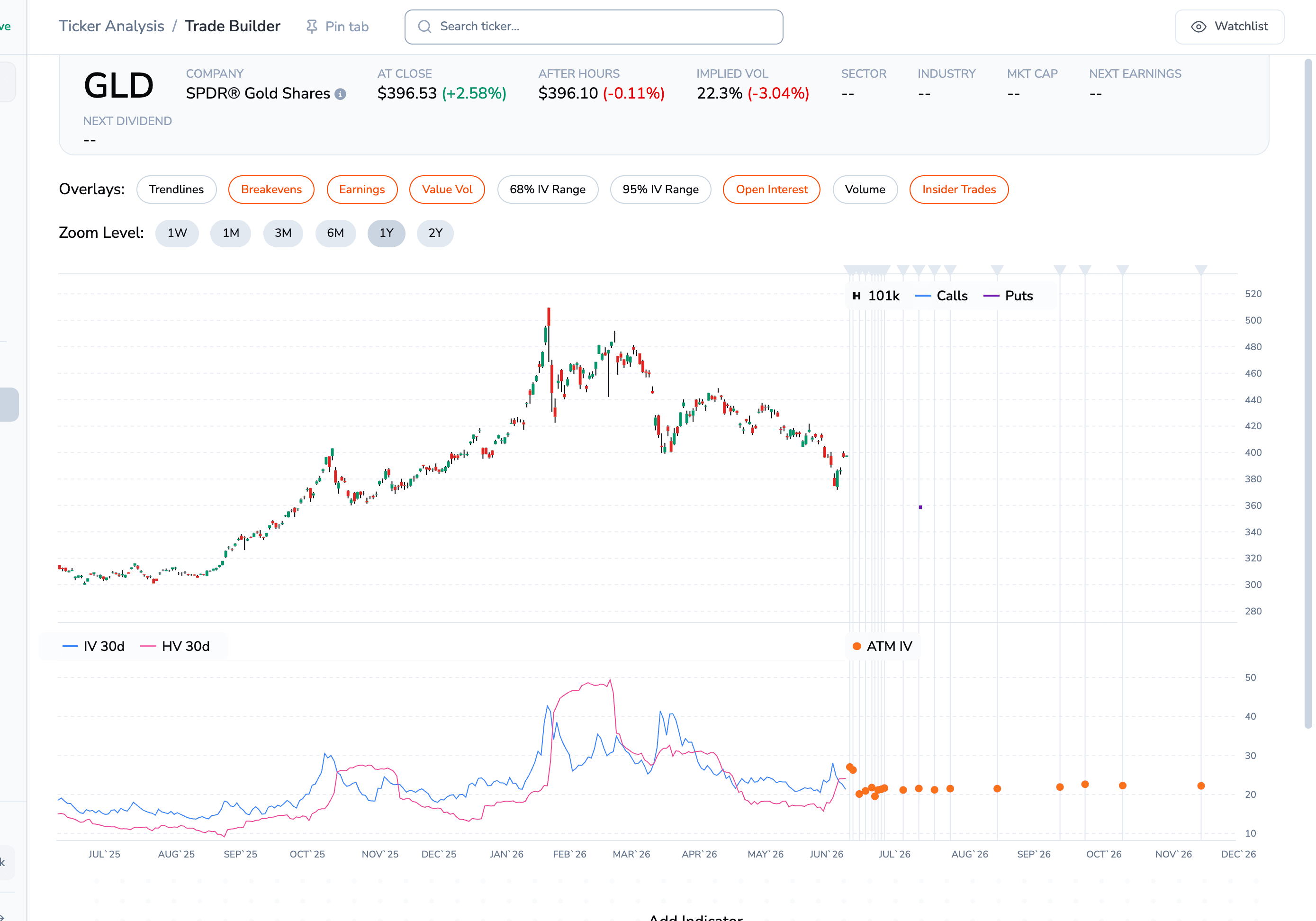

GLD's implied vol had already spiked to about 43% as gold went parabolic into the January 29 top, roughly double the 22% it had averaged over the prior year, and bled back toward that level as the metal fell.

GLD implied vs historical vol, ORATS Trade Builder

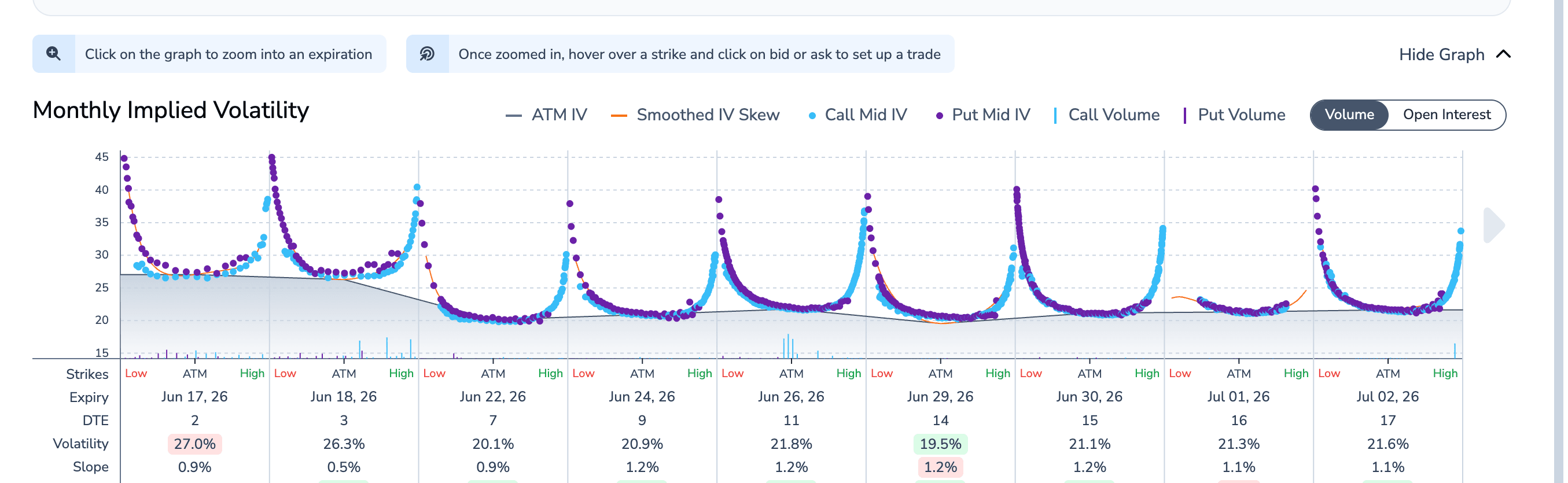

In the options chain, every monthly expiry now carries a positive slope, a put skew. Separately, the June 17 FOMC-day expiry is bid to 27% against about 20% a week out on event risk.

GLD monthly vol smiles and per-expiry skew, ORATS Options Chain

Two caveats keep it honest. This is about which wing is bid, not the level: gold's overall implied vol is only mid-range. And gold's put skew is mild next to equities, a +1.15 slope against the S&P's roughly +6, so this is gold dropping its upside bet, not pricing a crash. The flip also rode a parabolic rally that needed an excuse to correct; Warsh was the trigger, not the whole cause. The options no longer treat gold as a one-way crisis hedge. Pull the skew yourself from the /datav2/hist/cores slope field or the Options Chain, and watch which wing the decision bids.

Disclaimer:

The opinions and ideas presented herein are for informational and educational purposes only and should not be construed to represent trading or investment advice tailored to your investment objectives. You should not rely solely on any content herein and we strongly encourage you to discuss any trades or investments with your broker or investment adviser, prior to execution. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. Option trading and investing involves risk and is not suitable for all investors.

All opinions are based upon information and systems considered reliable, but we do not warrant the completeness or accuracy, and such information should not be relied upon as such. We are under no obligation to update or correct any information herein. All statements and opinions are subject to change without notice.

Past performance is not indicative of future results. We do not, will not and cannot guarantee any specific outcome or profit. All traders and investors must be aware of the real risk of loss in following any strategy or investment discussed herein.

Owners, employees, directors, shareholders, officers, agents or representatives of ORATS may have interests or positions in securities of any company profiled herein. Specifically, such individuals or entities may buy or sell positions, and may or may not follow the information provided herein. Some or all of the positions may have been acquired prior to the publication of such information, and such positions may increase or decrease at any time. Any opinions expressed and/or information are statements of judgment as of the date of publication only.

Day trading, short term trading, options trading, and futures trading are extremely risky undertakings. They generally are not appropriate for someone with limited capital, little or no trading experience, and/ or a low tolerance for risk. Never execute a trade unless you can afford to and are prepared to lose your entire investment. In addition, certain trades may result in a loss greater than your entire investment. Always perform your own due diligence and, as appropriate, make informed decisions with the help of a licensed financial professional.

Commissions, fees and other costs associated with investing or trading may vary from broker to broker. All investors and traders are advised to speak with their stock broker or investment adviser about these costs. Be aware that certain trades that may be profitable for some may not be profitable for others, after taking into account these costs. In certain markets, investors and traders may not always be able to buy or sell a position at the price discussed, and consequently not be able to take advantage of certain trades discussed herein.

Be sure to read the OCCs Characteristics and Risks of Standardized Options to learn more about options trading.

Related Posts