Indicators

Saturday, March 20th 2021

Answers To Common Questions: Calculating Skew

ORATS smoothing process produces important options metrics such as theoretical values, greeks, implied volatilities and summarizations of skew.

Summary

ORATS offers historical near end-of-day quotes back to 2007 via FTP for a special price of $399 per year for updating files daily plus only $399 one time fee for initial bulk download. The smoothed market values (SMV) process produces theoretical values, greeks, implied volatilities and summarizations of skew. The SMV process cleans quotes, applies good inputs to a modified binomial pricing engine, and fits a non-arbitrageable smooth curve through the strike implied volatilities. The benefits of smoothing include more consistent greeks, better summarizations of the skew, and the ability to compare call and put theoretical values to market bid-ask quotes.

User feedback is critical to helping us ensure top-quality tools and data. Answers to common questions will be a series of blog posts with our answers.

What Historical Quotes Available and Pricing?

Historical near end-of-day quotes back to 2007 via FTP are available for a special price of $399 per year for updating files daily plus only $399 one time fee for initial bulk download.

For students a half price rate is available for a special $299 per year of updates and a $299 one time for bulk.

We offer 15-minute delayed 1-minute snapshots for $99 per month, and offer history back to June 2020 for $499. Here is a large download of a sample of a 1-minute intraday snapshot. Here is a small snippet CSV of the first few rows.

Here is a large download of a sample 2-minute file (raw no greeks) that we have historically back to 2015: Nightly updates are $99 per month and bulk download back to 2015 is $999.

The instructions for users to set up an S3 bucket on Amazon Web Services to deliver of the 1-minute snapshots and 2-minute files require are in the links.

More information on our quotes is here https://info.orats.com/quotes

How does smoothed market values (SMV) process work?

After the SMV process is complete, ORATS calculates the quadratic fit parameters slope and derivative (skewness and kurtosis) on the smoothed implied volatilities. So the 3-point quadradic fits are not a seed or basis for our theoretical SMVs, but benefit from the SMV process. Here's how the SMV process works:

The SMV process

The first step in the SMV System is cleaning the quotes and applying good inputs to our modified binomial pricing engine. Using ORATS popular dividend feed and option pricing methodologies, a residual yield is solved for based on the put-call parity formula. Applying the residual yield rate process helps with summarizing hard-to-borrow stocks or stocks with differing dividend assumptions. The effect is to line up the call and put implied volatilities.

Next, using the call and put mid-price IVs, a non-arbitrageable smooth curve is fit through the strike implied volatilities.

- We use a proprietary skew generator using bounded flexible spline bands.

- We adjust the skews with another process to account for wings that may be slightly off put-call parity.

- We eliminate calendar or butterfly arbitrage in our theoretical values.

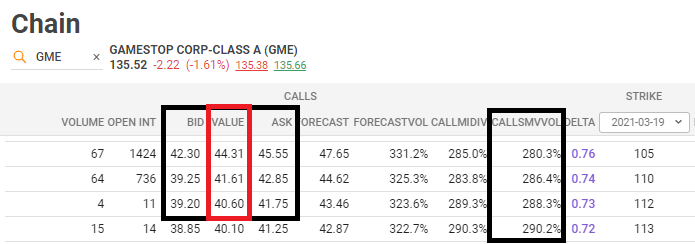

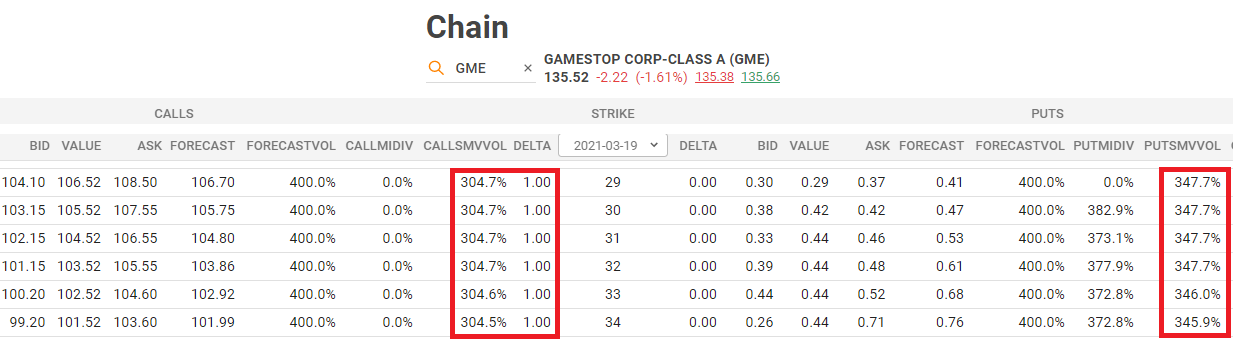

For example, in the Implied Monies endpoint for GameStop (GME) the residual yield represents the borrow rate that short sellers need to pay. The SMV process also calculates a confidence from 0 to 1 based on the amount of options implied volatilities and width of the market. Notice the higher confidence and lower market width in volatility points (mwVol) are related in the table below.

GME's borrow peaked at 93% before coming down and then rising again to today's level of 12% for the expirations around 30 days to expiration.

- SMV volatilities produce theoretical values that are between the bid-ask over 99% of the time.

Benefits of smoothing

Smooth market volatilities (SMV) derived from the options market helps traders make sense of a plethora of exchange quotes. There are three main benefits of smoothing the implied volatility skew:

- Call and put theoretical values can be compared to market bid-ask quotes to see if the options are under or overpriced.

- The smoothed IVs produce more consistent greeks that are important for backtesting, trading and managing risk.

- Smoothing the IVs create better summarizations of the skew.

This smoothing system produces powerful theoretical values and accurate option Greeks. The Strikes Report shows each option's bid-asks, greeks and theoretical values. Delta, Vega, Theta, Rho, Phi and theoretical values are critical for risk management and trading.

Benefits of 3-factor parameters

By parameterizing the smoothed curve, the shape can be evaluated comparing to other tickers, to history and to forecasts of the skew parameters.

We calculate quadratic fit parameters slope and derivative (skewness and kurtosis) but these are a result, not a seed or basis for our theoretical SMVs. Slope and derivative levels can be used as an entry point or exit point trigger in the backester, as can 100s of our historical calculations.

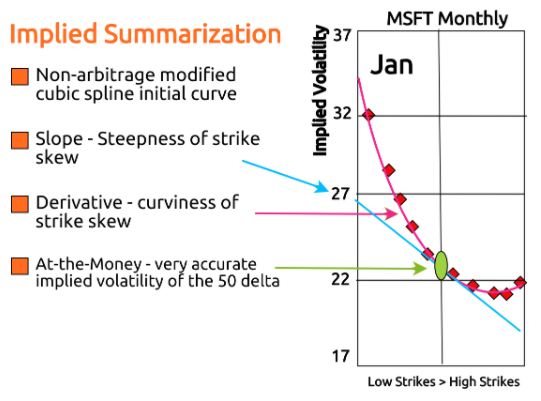

ORATS describes the implied volatility surface as a 3-dimensional surface where the independent variables are time to expiration, and option delta and the dependent variable is implied volatility. To illustrate an implied volatility surface, we have developed a 2-dimensional graph that displays all three axes in the figure below. Summary information about this surface gives the trader a macro view of the implied volatilities for each option chain.

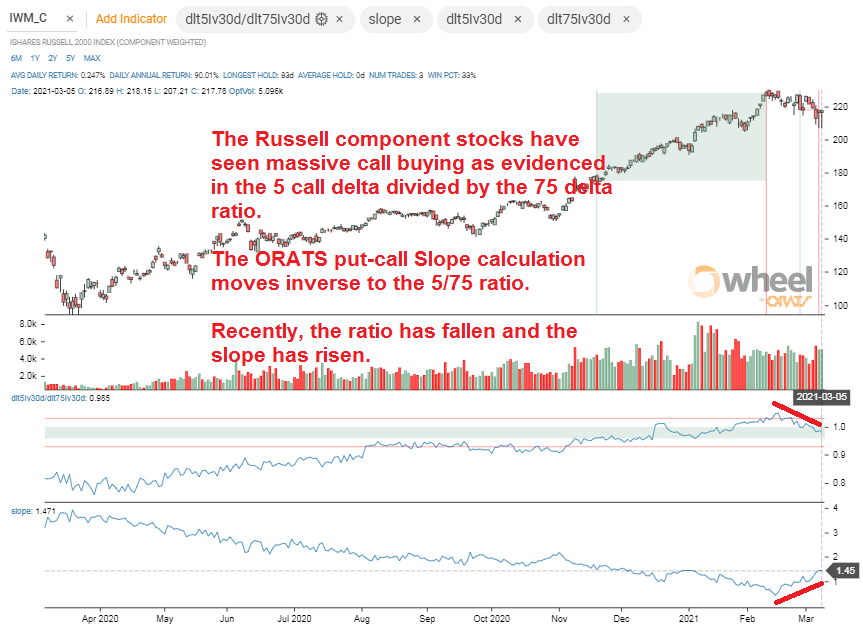

The importance of Slope can be seen in the graph below.

The importance of derivative (sometimes called kurtosis or curvature of the skew) has been seen lately, and in our view is the reason VIX is high compared to other implied volatility measurements. See our blog post here about that.

Question about wings, far OTM options

As can be seen below, the SMV volatilities are not capped until approaching the 1.00 or 0.00 delta wings. This can be seen in the strikes endpoint in our Data API or in Chain at wheel.orats.com

ORATS SMV also differentiates itself is by producing meaningful analytics on thinly traded securities and far out of the money options. The SMV incorporates historical information when the current confidence in the market summarization is low.

Moreover, the SMV treatment of the wings, the small delta out of the money calls and puts, produces more realistic implied volatilities than unadjusted IVs based on bid-ask prices with little premium.

ORATS data including skew information can be accessed via instructions at docs.orats.io and our API Explorer is a handy tool and can be found here.

We create second-order calculations like constant maturity volatilities, best ETF IV ratios, and others too numerous to state here (for example, five delta implied volatility 20 days to maturity with earnings effects taken out), but all are integrated into a trigger system where the data point or ratios of data points can be used to time trading in our backtest and live scanning at wheel.orats.com

We think our data has the best summarizations out there. You can check ours against others at this site https://quantpedia.com/links-tools/?category=historical-data

See our blog and others here on Feedspot.com's options trading blogs.

Disclaimer:

The opinions and ideas presented herein are for informational and educational purposes only and should not be construed to represent trading or investment advice tailored to your investment objectives. You should not rely solely on any content herein and we strongly encourage you to discuss any trades or investments with your broker or investment adviser, prior to execution. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. Option trading and investing involves risk and is not suitable for all investors.

All opinions are based upon information and systems considered reliable, but we do not warrant the completeness or accuracy, and such information should not be relied upon as such. We are under no obligation to update or correct any information herein. All statements and opinions are subject to change without notice.

Past performance is not indicative of future results. We do not, will not and cannot guarantee any specific outcome or profit. All traders and investors must be aware of the real risk of loss in following any strategy or investment discussed herein.

Owners, employees, directors, shareholders, officers, agents or representatives of ORATS may have interests or positions in securities of any company profiled herein. Specifically, such individuals or entities may buy or sell positions, and may or may not follow the information provided herein. Some or all of the positions may have been acquired prior to the publication of such information, and such positions may increase or decrease at any time. Any opinions expressed and/or information are statements of judgment as of the date of publication only.

Day trading, short term trading, options trading, and futures trading are extremely risky undertakings. They generally are not appropriate for someone with limited capital, little or no trading experience, and/ or a low tolerance for risk. Never execute a trade unless you can afford to and are prepared to lose your entire investment. In addition, certain trades may result in a loss greater than your entire investment. Always perform your own due diligence and, as appropriate, make informed decisions with the help of a licensed financial professional.

Commissions, fees and other costs associated with investing or trading may vary from broker to broker. All investors and traders are advised to speak with their stock broker or investment adviser about these costs. Be aware that certain trades that may be profitable for some may not be profitable for others, after taking into account these costs. In certain markets, investors and traders may not always be able to buy or sell a position at the price discussed, and consequently not be able to take advantage of certain trades discussed herein.

Be sure to read the OCCs Characteristics and Risks of Standardized Options to learn more about options trading.

Related Posts