Indicators

Monday, February 25th 2019

How ORATS Removes Earnings Effect from Implied Volatility

It's important to remove the effect of earnings announcements on implied volatility (IV). Normalizing IV allows for a better way to study it historically and compare cross-sectionally. Here's how we do it.

Summary

ORATS has a method for removing the effect of earnings announcements on implied volatility (IV) in order to better study it historically and compare cross-sectionally. This involves making accurate IV calculations, applying accurate earnings announcement dates, solving for an implied earnings effect, and presenting monthly and constant maturity readings historically. By isolating just the ex-earnings IV, valuable information baked into IV is not lost. The article provides examples of how this is done for TSLA and LULU.

ORATS has a way to remove the effect of earnings announcements on implied volatility (IV).

Normalizing IV allows for a better way to study it historically and compare cross-sectionally. For example, in the days before an earnings announcement, IV can rise as much as 50% in the front month expirations. Much of this rise is due to traders expecting a large move after announcement. If observers are not able to remove this effect, the valuable information baked into IV may be lost.

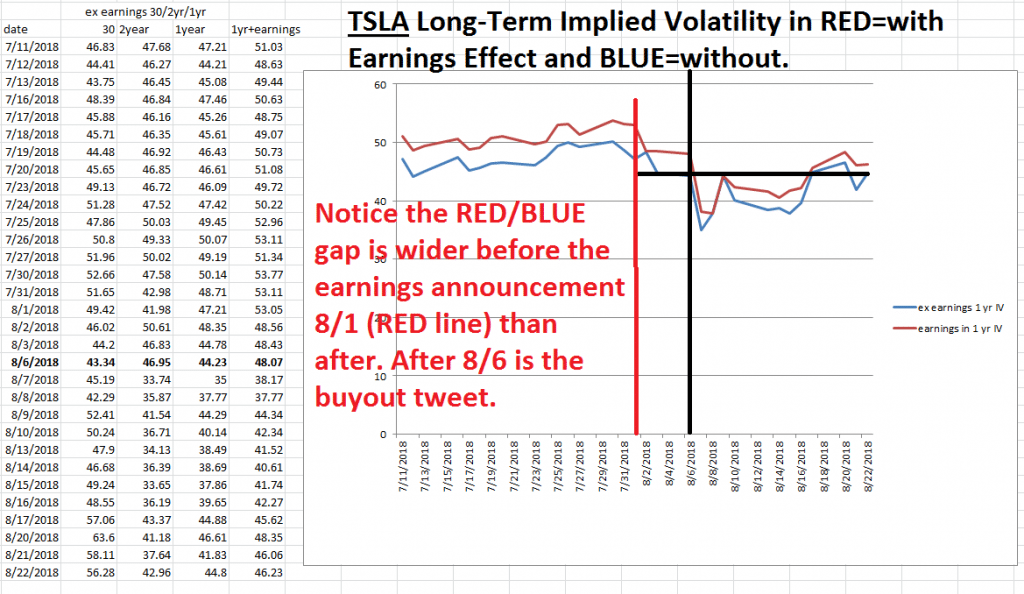

Consider TSLA below where earnings were announced on 8/1 and after the gap between the IV with and without earnings narrowed in the graph below. This is why it is important to isolate just the ex-earnings IV if analyzing implied volatility over time.

To remove the implied earnings effect in the IV, ORATS follows these steps.

- Make accurate implied volatility calculations by using accurate inputs like interest, dividends and residual rates;

- Apply accurate earnings announcement dates to determine how many earnings apply to each expiration;

- Solve for an implied earnings effect that makes the most rational resultant monthly implied volatility relationships;

- Present monthly and constant maturity readings historically.

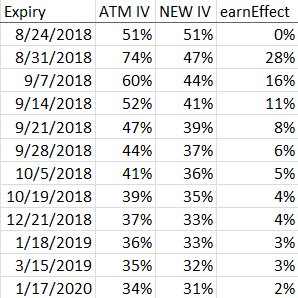

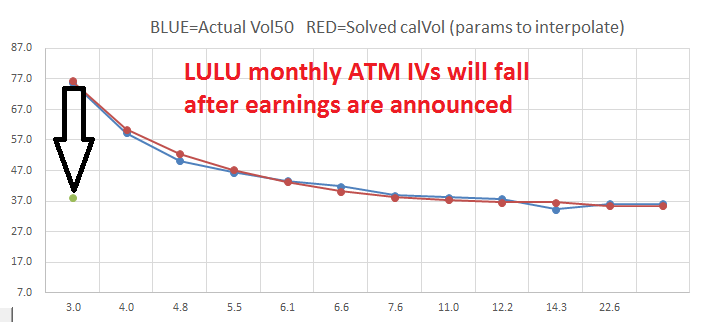

For example, consider LULU that announces earnings 8/30/2018 after the close. Presented below is the method for extracting earnings from IV. See the at-the-money IVs for each expiration, post removal of earnings effect IV, and that portion of the IV that is applicable to the earnings announcement move:

The 8/25/2018 expiry does not have an earnings effect. 8/31/2018 has the largest earnings effect (since the earnings effect will have a greater percentage of days relative to the number of days to expiration). Notice how the method solves for a remaining NEW IV skew that is still down sloping (backwardation).

The earnings effect is not the same as the percentage earnings move implied by the ATM IV relationships. In our Core Data API the percentage move implied from the options pricing for LULU is 10.93%.

Here are the last 12 actual earnings moves and the average absolute earnings move 11.698% to compare to the 10.93% Implied Earnings Move:

Disclaimer:

The opinions and ideas presented herein are for informational and educational purposes only and should not be construed to represent trading or investment advice tailored to your investment objectives. You should not rely solely on any content herein and we strongly encourage you to discuss any trades or investments with your broker or investment adviser, prior to execution. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. Option trading and investing involves risk and is not suitable for all investors.

All opinions are based upon information and systems considered reliable, but we do not warrant the completeness or accuracy, and such information should not be relied upon as such. We are under no obligation to update or correct any information herein. All statements and opinions are subject to change without notice.

Past performance is not indicative of future results. We do not, will not and cannot guarantee any specific outcome or profit. All traders and investors must be aware of the real risk of loss in following any strategy or investment discussed herein.

Owners, employees, directors, shareholders, officers, agents or representatives of ORATS may have interests or positions in securities of any company profiled herein. Specifically, such individuals or entities may buy or sell positions, and may or may not follow the information provided herein. Some or all of the positions may have been acquired prior to the publication of such information, and such positions may increase or decrease at any time. Any opinions expressed and/or information are statements of judgment as of the date of publication only.

Day trading, short term trading, options trading, and futures trading are extremely risky undertakings. They generally are not appropriate for someone with limited capital, little or no trading experience, and/ or a low tolerance for risk. Never execute a trade unless you can afford to and are prepared to lose your entire investment. In addition, certain trades may result in a loss greater than your entire investment. Always perform your own due diligence and, as appropriate, make informed decisions with the help of a licensed financial professional.

Commissions, fees and other costs associated with investing or trading may vary from broker to broker. All investors and traders are advised to speak with their stock broker or investment adviser about these costs. Be aware that certain trades that may be profitable for some may not be profitable for others, after taking into account these costs. In certain markets, investors and traders may not always be able to buy or sell a position at the price discussed, and consequently not be able to take advantage of certain trades discussed herein.

Be sure to read the OCCs Characteristics and Risks of Standardized Options to learn more about options trading.

Related Posts